If you've been searching for a home in the Denver metro or Colorado foothills this year, you already know affordability is still the story. Rates haven't come down as fast as most buyers hoped, and the gap between what people want to spend and what homes are actually listed for remains very real across markets like Evergreen, Littleton, Arvada, and Golden.

That's a big part of why adjustable-rate mortgages — ARMs — are getting a second look from Colorado home buyers who want to get into the market now without pushing their monthly budget past the breaking point. In fact, the share of buyers choosing ARMs has been steadily climbing over the last couple of years.

Here's a plain-language breakdown of how ARMs work, why more buyers are choosing them, and what you should think carefully about before going that route.

What Is an Adjustable-Rate Mortgage?

Most people are familiar with the 30-year fixed mortgage — your rate stays locked for the life of the loan, and your principal and interest payment doesn't budge. Taxes and homeowner's insurance can still move the needle on your total monthly payment, but the core of what you owe the lender each month stays steady.

An adjustable-rate mortgage works differently. You get a fixed rate for an initial period — often five or seven years — and after that, the rate adjusts periodically based on market conditions. If rates have gone up, your payment goes up. If they've come down, your payment could drop.

The trade-off is simple: more certainty with a fixed loan, more upfront savings potential with an ARM. Which one makes sense depends entirely on your situation.

Why ARMs Are Getting More Attention Right Now

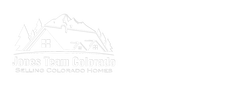

The appeal is straightforward: ARM rates are typically lower than 30-year fixed rates, which means a lower monthly payment right out of the gate. And according to data from Mortgage News Daily and the Wall Street Journal, that gap is real and meaningful right now.

According to Redfin, the typical buyer could save around $150 per month by choosing an ARM over a 30-year fixed mortgage at today's rate spread. Over the course of a year, that's $1,800 — real money that some buyers are using to offset closing costs, build savings, or simply maintain a more comfortable budget while they get settled.

For Colorado buyers watching home prices in the $700K–$1.2M range — a common target in Jefferson County and the foothills communities — even a modest reduction in monthly payment can shift the math enough to make a purchase workable.

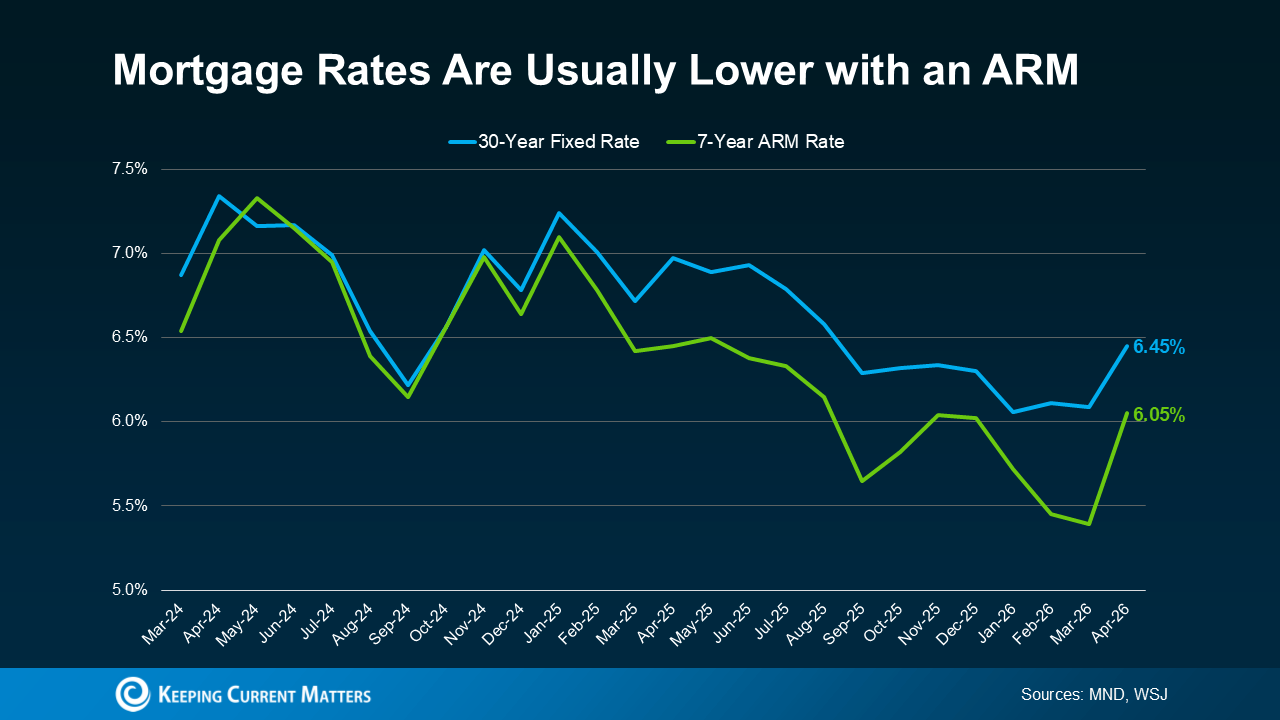

More Buyers Are Choosing ARMs — and That's Not a Red Flag

Data from the Mortgage Bankers Association shows the share of buyers opting for ARMs has been climbing steadily, especially over the last few years as fixed rates stayed elevated.

If that trend gives you a sense of déjà vu from 2005–2007, that's understandable. But today's market is very different from the run-up to the housing crash. Back then, many buyers were approved for ARM loans they couldn't realistically afford once the rate adjusted — and lending standards were loose enough to let that happen at scale.

Today, underwriting is considerably more rigorous. Lenders now evaluate whether a borrower could handle the payment even if rates rise. So while ARMs are gaining popularity again, this isn't a warning sign — it's simply buyers adapting creatively to a high-rate environment. Colorado's market is no different from the national trend in that regard.

The Trade-Off: What Colorado Buyers Need To Think Through

An ARM isn't right for every buyer, and in Colorado's foothills and mountain communities, there are a few additional considerations worth weighing.

An ARM may make sense if:

You plan to sell or move within the initial fixed-rate period — perhaps a transitional home while you settle into Colorado, or a step-up property you expect to outgrow in five to seven years. It can also make sense if your income is likely to increase significantly in the years ahead, giving you more cushion when the rate eventually adjusts.

Where to be careful:

Once the fixed period ends, your rate can adjust — and there's no guarantee of where rates will be at that point. If you're buying your forever home in Morrison, Conifer, or Pine with plans to stay put for 15-plus years, a fixed rate gives you a baseline you can plan around for the long haul. Refinancing later is always an option in theory, but it's not guaranteed — rates could stay flat or move higher, and transaction costs eat into any savings.

The honest bottom line: your risk tolerance matters as much as the math. If the possibility of a higher payment in year six or seven would create real stress, the peace of mind that comes with a fixed rate may be worth the higher starting payment.

Bottom Line for Colorado Buyers

ARMs are a legitimate tool in a high-rate environment, and they deserve a real conversation — not a reflex "no." The $150/month savings Redfin cites may not sound dramatic, but compounded over a five-year initial period, and applied against a Denver-area home price, it adds up quickly. For the right buyer with the right timeline, an ARM can be a smart move.

But they're not for everyone, and the best decision always starts with a trusted lender — someone who can walk you through the actual numbers on a specific loan, your specific income, and your specific five- to ten-year plan.

Tim and Sandy Jones work closely with buyers across the Denver metro, Jefferson County, and the foothills every day. If you're trying to figure out whether buying now makes sense — with an ARM, a fixed loan, or just exploring your options — we're happy to connect you with trusted local lenders and help you think through the full picture.

Frequently Asked Questions: ARMs and Colorado Home Buyers

What does a 5/1 ARM mean for a Colorado home buyer?

A 5/1 ARM means your interest rate is fixed for the first five years, then adjusts once per year after that based on a benchmark index plus a margin set by your lender. The "5" is how long the initial fixed period lasts; the "1" is how often it adjusts after that. A 7/1 ARM follows the same structure but gives you seven years of payment stability before adjustments begin.

Are adjustable-rate mortgages risky in today's Colorado market?

They carry more uncertainty than a fixed loan, but today's ARMs come with caps that limit how much your rate can rise in any single adjustment and over the life of the loan. That's very different from the pre-2008 era. The key is understanding those caps, knowing your timeline, and making sure your budget can absorb a higher payment if it comes to that.

How much can I save monthly with an ARM on a Denver-area home?

According to Redfin, the national average is roughly $150 per month. At higher price points common in the Denver metro and Jefferson County — say $800K to $1.2M — that savings can be more meaningful since the loan amount is larger. Your actual savings will depend on the specific loan, lender, and current rate spread at the time you lock.

Should I wait for fixed rates to drop, or buy now with an ARM?

That depends on your situation, and there's no universal right answer. What we've seen consistently in the Colorado market is that buyers who wait for the "perfect rate" often find themselves competing against more buyers when rates do drop — which tends to push prices up. An ARM lets some buyers get into the market now while keeping the monthly payment manageable, with the option to refinance later if conditions improve.

Ready to Talk About Your Move in Colorado?

Whether you're thinking about buying, selling, or just want a straight answer about what the market looks like right now, Tim and Sandy Jones are here to help — no pressure, no sales pitch.

📧 [email protected]

📞 (720) 314-8462 — call or text anytime

📅 Schedule a free 15-minute call

Check out this article next